From April 1, 2025, it is mandatory for all taxpayers, irrespective of turnover, to use Two-Factor Authentication system for e-invoice and e-way bill generation.

| Photo Credit: Vaishali R Venkat

The Story so far: The GST Council of India approved and rolled out the ‘e-invoicing’ or ‘electronic invoicing’ eco-system in a phased manner for reporting of business-to-business (B2B) invoices to GST portal. As there were no existing standards/formats then, a standardised format was introduced across the country, after having several consultations with trade/industry bodies as well as Institute of Chartered Accountants of India. Since then, several changes were also being made to the GST e-invoicing rules and regulations. Before getting into the details of what is GST e-invoicing and how this works, let’s first check out the new rules.

New rules from April 1, 2025:

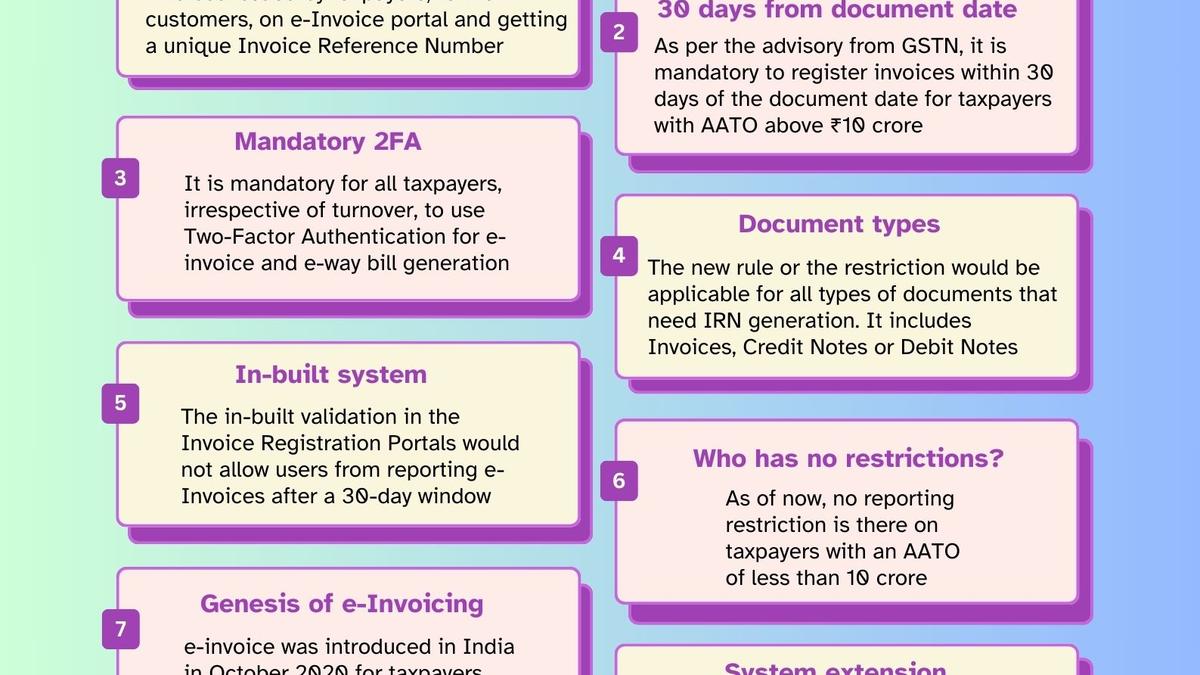

From April 1, 2025, business houses with an Annual Aggregate Turn Over (AATO) of ₹10 crore and above must report/upload e-invoices to the Invoice Registration Portal (IRP) within 30 days from the date of issue of the document. Earlier, this rule was meant only for business houses with an AATO of more than ₹100 crore. As the turnover threshold has been reduced drastically, large number of business houses must comply with this 30-day deadline.

Currently, there are no strict regulations on the deadline of reporting invoices. Therefore, a few businesses upload invoices in a delayed manner, thereby creating discrepancies in Input Tax Credit (ITC) claims and overall tax compliance. But now, the in-built validation in the IRPs would not allow users from reporting e-Invoices after the 30-day window. Late submissions would automatically be rejected, with consequences leading to potential penalties and financial setbacks.

Compulsory Two-Factor Authentication

From April 1, it is mandatory for all taxpayers, irrespective of turnover, to use Two-Factor Authentication (2FA) system for e-invoice and e-way bill generation.

What is GST e-invoicing?

GST e-invoicing involves reporting of B2B invoices and export invoices issued by taxpayers, to their customers, on the Union Government’s e-invoice portal and getting a unique Invoice Reference Number (IRN). This doesn’t mean that the invoice would be generated by the government portal itself. Further, e-invoice doesn’t simply mean that the invoice would be in a soft copy version such as PDF. According to the GST portal, “It’s a faceless system with major thrust on API integration so that the eco-system can exchange the data electronically.”

When was it approved and rolled out?

The standard of GST e-invoice was first approved by the GST Council in its 37th meeting held on September 20, 2019. e-Invoicing was introduced in India, in a phased manner, in October 2020 for taxpayers with Annual Aggregate Turn Over (AATO) of more than ₹500 crore. Later, in January 2021, the eco-system was extended to taxpayers with AATO between ₹100 and ₹500 crore.

What are the documents to be uploaded?

The types of documents that need to be uploaded for IRN generation include GST Invoices, Credit Notes or Debit Notes related to B2B supplies and exports.

Which business houses are exempted?

Special Economic Zone (SEZ) units, insurance and banking sectors including non-banking financial companies (NBFCs), multiplex cinema admissions, goods transport agency [transporting goods by road in carriage] and passenger transport services.

What is the e-invoicing process?

To begin with, taxpayers would keep creating GST invoices as usual in their own accounting/billing/ERP systems, during the course of their business. Once this process is completed from their end, the invoices created by them would then be reported to the Invoice Registration Portal (IRP). After the report is made by the taxpayers, the IRP would return a signed e-invoice with a Unique Invoice Reference Number (IRN) with a QR code. Then, the invoice with the QR code would be issued. It may be noted that a GST invoice would be valid only with a valid IRN.

What are the advantages?

The e-invoice system has many benefits for business houses. For instance, the invoice details would be automatically populated into GST return forms or e-way bill forms, thus reducing time and labour. Further, it helps in the reduction of disputes and processing costs, as all forms are digitally stored. It helps in improving payment cycles, thus enhancing business efficiency. The system uses standardised and digitally verifiable e-invoice format, based on international standards (UBL/PEPPOL). This enhances machine readability, interoperability and uniform interpretation in the e-invoicing eco-system across the board. Owing to these Interoperable services, tax payers could seamlessly switch over from one portal to other.

Further, with the help of GST e-invoice system fraudulent actions/transactions by a few unscrupulous taxpayers would be curbed. There would be considerable reduction in fraud cases as tax authorities have access to real-time data.

What tools are available?

e-Invoices can be reported in multiple modes and taxpayer can choose any one of the tools they are comfortable with. The available tools are: API interface, mobile app, GST e-Invoice Preparing and Printing (GePP) tool (web based online/offline modes), bulk upload tool etc.

Published – April 01, 2025 07:00 am IST